How restaking security creates yield

EigenLayer introduces a mechanism that allows stakers to reuse their Ethereum security for multiple purposes simultaneously. When you stake ETH, you are providing cryptoeconomic security to the base layer. Restaking allows you to direct that same security toward Actively Validated Services (AVSs) without needing to lock up additional capital. This reuse of security is the foundation for new revenue streams beyond standard staking rewards.

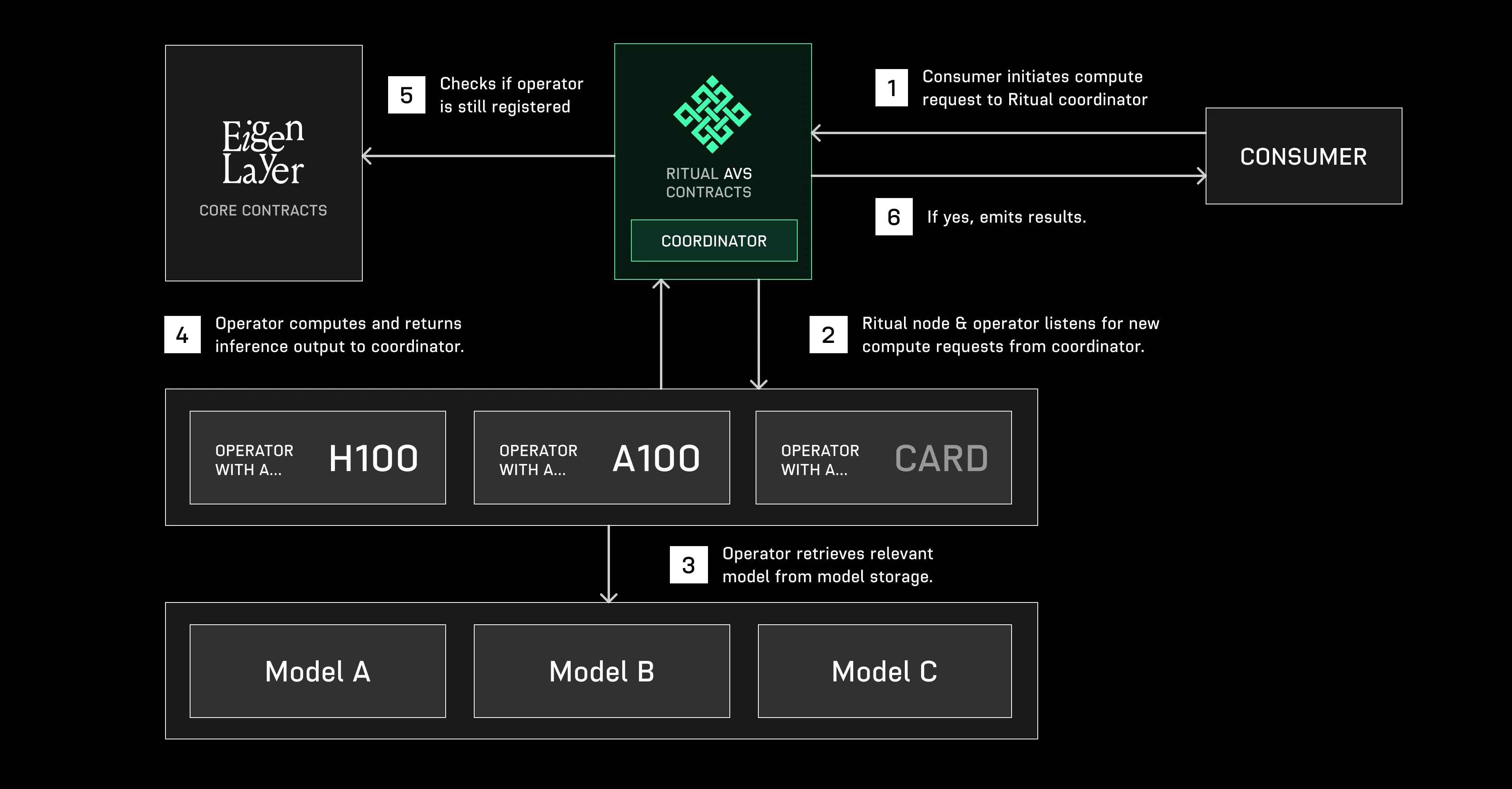

An AVS is a decentralized service built on Ethereum that requires its own consensus layer. Examples include data availability layers, oracle networks, bridges, and coprocessors. These services need security to function, but building a dedicated validator set is expensive. EigenLayer solves this by letting AVSs tap into Ethereum's existing security pool. Operators who run the infrastructure for these services earn fees from AVS consumers, which are distributed back to the restakers.

This model amplifies Ethereum's security while offering stakers enhanced rewards. Instead of choosing between securing the base layer or supporting new applications, restakers can do both. The yield generated comes from the fees paid by AVS consumers for using these services. This creates a direct link between the utility of new decentralized applications and the returns for ETH stakers.

How Operators Price Validation Services

EigenLayer’s revenue model rests on a direct transactional relationship between operators and AVS consumers. Operators provide the computational and cryptographic resources required to secure these services, charging fees that reflect the cost of running validator nodes and the market demand for specific security guarantees. This pricing structure determines how much value flows back to restakers who have delegated their stake to these operators.

The primary revenue source is the service fee paid by AVS consumers. These fees compensate operators for the bandwidth, storage, and compute power needed to validate transactions or attest to state roots. In markets like data availability or oracle networks, fees are often volume-based, scaling with the number of transactions or data blocks processed. For consensus-heavy services like shared sequencers, fees may be fixed or tiered based on priority and latency requirements.

These fees are collected in the native token of the AVS or in ETH, depending on the smart contract implementation. Once collected, the operator deducts a performance fee—typically ranging from 10% to 20%—before distributing the remainder to restakers. This distribution is automated via EigenLayer’s smart contracts, ensuring that restakers receive proportional rewards based on their delegated stake.

The sustainability of this model depends on the AVS’s ability to generate consistent demand. If an AVS fails to attract users, operators may lower fees to remain competitive, compressing margins for restakers. Conversely, high-demand services can command premium rates, offering higher yields for those who delegate to reputable operators. This dynamic creates a meritocratic market where operator reputation and technical reliability directly influence earning potential.

Data availability and sequencer models

Data availability (DA) networks and shared sequencers represent the highest-revenue tier of EigenLayer AVSs in 2026. These services command premium fees because they solve foundational infrastructure bottlenecks: storing massive amounts of off-chain data and coordinating transaction ordering across multiple chains.

Unlike oracle networks or bridges, which often compete on price, DA and sequencer AVSs function as critical utility layers. They capture value through volume-based pricing models, where fees scale directly with the data throughput or transaction load they secure. This structural demand creates more predictable and higher-margin revenue streams for restakers.

The table below compares the revenue potential and risk profiles of these top-tier AVS categories against other common EigenLayer services.

| AVS Category | Primary Revenue Driver | Security Risk | 2026 Maturity |

|---|---|---|---|

| Data Availability (DA) | Volume-based storage fees | High (slashing events impact many chains) | High |

| Shared Sequencers | Transaction ordering premiums | High (centralization trade-offs) | Medium-High |

| Oracle Networks | Per-query or subscription fees | Medium (data accuracy errors) | High |

| Cross-Chain Bridges | Transaction fees + spread | Very High (smart contract exploits) | Medium |

How Yield Flows from AVS to Restakers

Understanding the mechanical flow of funds is essential for evaluating the risk-adjusted return of restaked capital. The distribution process is not a passive accumulation but a series of on-chain settlements governed by EigenLayer’s smart contracts and the specific logic of each Autonomous Verifiable Service (AVS).

1. Service Provision and Fee Generation

An AVS consumes Ethereum’s shared security to perform off-chain or parallelized tasks, such as data availability or oracle verification. The consumers of these services—dApps, protocols, or users—pay fees in ETH or native tokens for this security. These fees accumulate in the AVS’s designated contract, forming the total revenue pool available for distribution.

2. Smart Contract Settlement

EigenLayer acts as the settlement layer, ensuring that the AVS correctly submits its state roots and proofs. Once the AVS contract confirms the validity of the work performed, it triggers a distribution call. The smart contract calculates the proportional share of fees owed to each restaker based on their staked ETH or Liquid Staking Tokens (LSTs). This calculation is automated and immutable, removing the need for manual payout reconciliation.

3. Direct Distribution to Restakers

The calculated yield is transferred directly to the restaker’s wallet or delegated operator. This flow is transparent; every transaction is recorded on Ethereum, allowing restakers to audit the incoming revenue against the fees charged by the AVS operator. The efficiency of this step depends on the AVS’s fee structure and the gas costs associated with the settlement transactions.

4. Slashing Risk and Capital Exposure

Yield distribution is contingent on continuous compliance. If an AVS operator acts maliciously or fails to provide the required verification, EigenLayer’s slashing mechanism can seize a portion of the restaker’s staked assets. This risk is the primary counterweight to high yields. Restakers must carefully assess the economic incentives and security guarantees of each AVS, as the potential for slashing directly impacts the net annual percentage yield (APY).

Evaluating AVS risk and return

Assessing the revenue sustainability of an Actively Validated Service (AVS) requires distinguishing between genuine utility and speculative token emissions. The primary metric for long-term viability is the presence of a consistent, external consumer base that pays for the service in stable value, rather than relying solely on protocol-incentivized demand.

A robust AVS framework must demonstrate clear demand from end-user applications. Whether providing data availability, oracle services, or shared sequencing, the service must solve a specific bottleneck for other protocols. Without this foundational utility, revenue streams are likely to evaporate once early incentive programs conclude.

Technical integrity is equally critical. Investors should verify that the AVS codebase is open-source and has undergone rigorous audit. Open repositories, such as the Ava Protocol implementation on GitHub, allow for independent verification of the consensus mechanism and slashing conditions. This transparency reduces the risk of hidden vulnerabilities that could compromise the security deposit.

To streamline this due diligence process, use the following checklist to vet potential AVS investments:

- Contract Audits: Confirm independent security audits are public and recent.

- Consumer Demand: Identify active dApps paying for the service’s output.

- Slashing History: Review on-chain data for any slashing events indicating operator misconduct or technical failure.

Common questions about EigenLayer AVS

What is an AVS in EigenLayer?

An Autonomous Verifiable Service (AVS) is a decentralized application built on Ethereum that leverages EigenLayer’s restaking mechanism to provide custom verification for off-chain operations. By sharing Ethereum’s cryptoeconomic security, AVSs can operate with enhanced decentralization and cost efficiency without building their own validator sets from scratch.

Who are AVS consumers?

AVS consumers are the end users or applications that utilize the services provided by an AVS. These services range from data availability layers and shared sequencers to oracle networks, bridges, and coprocessors. The consumer interacts with the AVS to access these specialized blockchain capabilities secured by restaked ETH.

What is an AVS in blockchain?

In the broader blockchain ecosystem, an AVS refers to protocols that require their own consensus layer to function, such as Layer 2 rollups, sidechains, or data availability networks. Unlike standard dApps, AVSs actively validate transactions or data, relying on EigenLayer’s shared security model to maintain integrity and prevent censorship.

What does EigenLayer do?

EigenLayer is a restaking protocol on Ethereum that allows stakers to reuse their staked ETH or liquid staking tokens (LSTs) to secure additional services. This mechanism amplifies Ethereum’s security footprint, enabling new decentralized applications to launch with robust validator support while offering stakers additional yield opportunities.

No comments yet. Be the first to share your thoughts!