How EigenLayer Restaking Works in 2026

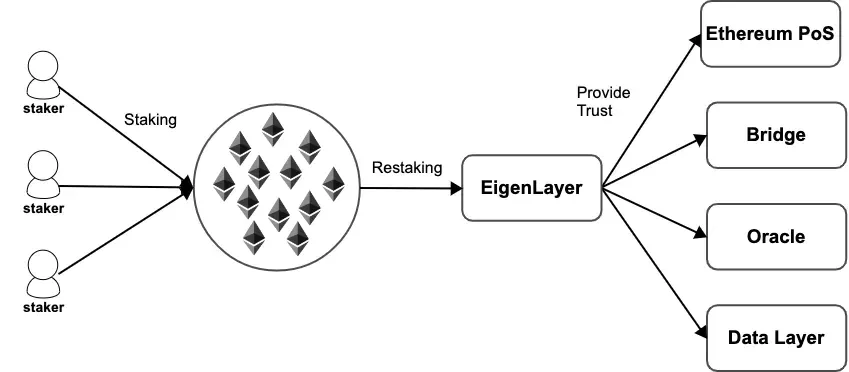

EigenLayer restaking has matured from a novel yield strategy into a foundational layer of Ethereum’s infrastructure. In 2026, the protocol operates as a shared security marketplace, allowing Ethereum validators to delegate their staked ETH to secure additional decentralized services. This mechanism, known as Actively Validated Services (AVS), transforms staking from a passive income stream into an active participation model for broader network security.

The core innovation lies in the unbonding of security. Validators no longer need to run separate nodes for every new protocol. Instead, they sign cryptographic attestations that prove their stake backs specific AVSs, such as oracles, data availability layers, or bridges. This creates a modular security economy where capital is reused efficiently. As noted by industry analysts, this shared security model is the defining infrastructure shift of the current cycle, enabling new applications to launch with institutional-grade security without building their own validator sets.

This architectural shift is underpinned by EIP-7251, which increased the maximum effective balance for a single validator from 32 ETH to 2,048 ETH. By allowing larger, more consolidated validator positions, the upgrade significantly reduces the operational overhead for running multiple AVS tasks. This consolidation is critical for 2026’s ecosystem, as it encourages professional node operators to participate in the AVS market, driving down costs and increasing the reliability of secured services.

The result is a more robust security substrate for Ethereum. While yield opportunities remain attractive, the primary value proposition in 2026 is the strengthening of the entire network’s defensive posture. EigenLayer restaking is no longer just about extracting yield; it is about contributing to the decentralized integrity of the broader crypto economy.

Comparing major liquid restaking tokens

Liquid Restaking Tokens (LRTs) have evolved from simple yield wrappers into complex financial primitives. While EigenLayer provides the underlying security layer, individual LRT protocols like Renzo, Kelp, and Puffer layer their own mechanics on top. This creates distinct differences in yield composition, fee structures, and liquidity options that matter for your portfolio.

The core trade-off is between simplicity and yield optimization. Some protocols prioritize high, variable yields by aggressively allocating to high-yield Active Validation Services (AVS), while others focus on capital preservation and lower volatility. Understanding these mechanical differences is essential before allocating capital.

Yield composition and risk profile

Yield from LRTs generally comes from three sources: base Ethereum staking rewards, EigenLayer restaking rewards, and additional AVS-specific incentives. Protocols differ significantly in how they balance these sources.

Puffer Finance, for example, often emphasizes capital efficiency and flexible withdrawal mechanisms, catering to users who want liquidity alongside yield. Renzo focuses on broad AVS diversification to spread risk across multiple networks. Kelp DAO (via RSETH) often leans into institutional-grade infrastructure and stable, predictable returns. These choices directly impact the risk-adjusted return you experience.

Fees and liquidity mechanics

Fees in the LRT space are not uniform. Some protocols charge a percentage of yield earned, while others have fixed management fees or no fees at all for certain tiers. Liquidity also varies: some LRTs are deeply integrated into decentralized exchanges (DEXs) like Uniswap, providing easy exit ramps, while others may have thinner liquidity pools.

Always check the current fee schedule and liquidity depth on the protocol’s official documentation. A high yield is meaningless if you cannot exit the position without significant slippage.

| Protocol | Primary Yield Source | Fee Model | Liquidity Depth |

|---|---|---|---|

| Renzo | AVS Diversification | Yield-based | High |

| Kelp (RSETH) | Stable Staking + AVS | Yield-based | Medium-High |

| Puffer Finance | Flexible AVS + Gas Optimization | Variable/None | Medium |

| Swell (swETH) | EigenLayer + Network Partnerships | Yield-based | High |

The table above summarizes the current structural differences. Note that yield sources and fee models are subject to change as AVS landscapes evolve. Always verify the latest parameters on the official protocol websites before interacting.

Understanding AVS Security and Slashing Risks

As EigenLayer solidified its position in 2026, holding roughly 94% of the restaking market with over $15 billion in staked assets, the protocol’s security model faced intense scrutiny. The primary concern for operators and restakers is not just the general stability of Ethereum, but the specific mechanics of Actively Validated Services (AVS). Each AVS operates with its own security parameters, creating a fragmented risk landscape where a failure in one service can trigger cascading penalties across the entire restaking ecosystem.

AVS-Specific Slashing Complexity

Unlike traditional staking, where slashing is governed by a single, uniform protocol rule, AVS slashing is modular. Each service defines its own misbehavior conditions and slashing criteria. This means an operator running multiple AVSs is exposed to a diverse set of slashing rules. A misconfiguration in one AVS’s smart contract or oracle feed can lead to significant financial penalties, even if the operator’s core Ethereum validator is performing correctly. The complexity lies in the fact that these rules are not standardized, requiring operators to maintain deep, service-specific knowledge to avoid accidental slashing.

Concentration Risk in a Dominant Protocol

The sheer market dominance of EigenLayer introduces a unique form of concentration risk. With the majority of restaked assets funneled through a single protocol, a systemic bug or exploit in EigenLayer’s core contracts could have catastrophic implications for the entire restaking market. This "too big to fail" dynamic means that the security of hundreds of dependent AVSs is tied to the integrity of one central infrastructure layer. While this concentration provides liquidity and ease of use, it also creates a single point of failure that critics argue undermines the decentralized ethos of Ethereum.

Mitigating Operator Risk

To navigate these risks, operators must adopt a more rigorous approach to AVS selection and configuration. This involves not only understanding the technical requirements of each service but also continuously monitoring their performance and the health of the underlying smart contracts. Diversifying across multiple AVSs with different security models can help mitigate the impact of a single failure, but it also increases operational complexity. Restakers must weigh the potential yield against the heightened risk of managing a more complex, multi-layered security posture.

Yield Breakdown: What Validators Actually Earn

EigenLayer restaking yield is not a single number but a composite of three distinct income streams. Understanding how these components stack is essential for calculating realistic returns and managing risk. The total yield generally consists of base ETH staking rewards, EigenLayer points, and incentives from Active Validation Services (AVSs).

Base ETH Staking Rewards

The foundation of restaking yield is the native ETH staking reward. When you stake ETH directly or through a Liquid Restaking Token (LRT), you earn the base protocol yield from Ethereum’s consensus layer. This yield is determined by the network’s total staked ETH and is relatively stable, currently hovering around 3-4% annually. This portion of the yield is non-negotiable and represents the baseline compensation for securing the Ethereum network.

EigenLayer Points

EigenLayer introduced a points system to incentivize early participation and liquidity provision. While points do not directly translate to cash yield, they are a critical proxy for future token rewards. Validators and restakers accumulate points based on their staked ETH and the duration of their commitment. Although the exact conversion rate to the $EIGEN token is still being finalized, these points represent a significant potential upside that can substantially boost overall returns beyond the base ETH yield.

AVS-Specific Incentives

The most variable and potentially lucrative component of restaking yield comes from Active Validation Services (AVSs). AVSs are third-party applications that leverage EigenLayer’s shared security to provide services like data availability, oracle networks, or decentralized compute. To attract validators, AVSs offer their own token incentives. These rewards can vary wildly depending on the AVS’s maturity, demand for its services, and tokenomics. For many validators, AVS incentives are the primary driver for choosing to restake rather than simply staking ETH directly.

Pre-Opt-In Checklist for Restakers

Before delegating ETH or liquid staking tokens to EigenLayer, validators and users must audit their technical and financial exposure. Restaking amplifies yield but also concentrates slashing risk across multiple Active Verification Services (AVS). Use this checklist to ensure your setup can withstand potential penalties.

Ensure your validator client supports slashing protection databases. Without this, a double-signing event could trigger penalties across both consensus and restaking layers. Tools like Holesky testnet validators often serve as the baseline for safe configuration.

Not all AVS carry the same threat level. Review the smart contract audits and economic security of each service you opt into. Prioritize AVS with proven track records and transparent governance over newer, higher-yield options.

Model your portfolio under worst-case slashing conditions. If multiple AVS slash simultaneously, does your remaining balance cover operational costs? Ensure you have sufficient buffer liquidity to maintain validator uptime.

If using LSTs like rETH or stETH, verify that the underlying protocol supports EigenLayer restaking. Some older LST versions may not be compatible with the latest restaking contracts, leading to failed transactions or locked funds.

Restaking interactions often require multiple transactions. Factor in Ethereum gas fees, which can spike during network congestion. Use a gas tracker to time your opt-in and opt-out actions for cost efficiency.

| Risk Factor | Impact | Mitigation |

|---|---|---|

| Slashing | High | Slashing protection databases |

| Smart Contract Bug | Critical | Audited AVS contracts |

| Gas Spikes | Low | Gas optimization tools |

The cost of restaking extends beyond yield; it includes the operational burden of managing multiple validator responsibilities. Regularly review your AVS portfolio and adjust your risk exposure as the ecosystem evolves.

No comments yet. Be the first to share your thoughts!